Navigating the complex world of American healthcare can feel like a full-time job, especially when you’re trying to find out if your glp-1 is covered by insurance. With medications like Wegovy and Zepbound retailing for over $1,000, insurance approval isn’t just a convenience it’s a necessity for many. If you’ve been denied coverage or are just starting the process, take a deep breath. You are not alone, and there is a proven path to success.

We understand the frustration of being told that a life-saving medication is “not covered.” Our “gut-check” tone is here to prioritize your safety and peace of mind by providing a transparent roadmap through the prior authorization (PA) maze. In this guide, we will explain the 2026 insurance landscape, reveal the criteria providers look for, and show you exactly how to appeal a denial so you can get the treatment you deserve at a price you can afford.

The 2026 landscape: who covers GLP-1s?

As of 2026, insurance coverage for GLP-1 medications is in a state of flux. While many commercial plans (like Blue Cross Blue Shield, UnitedHealthcare, and Aetna) have expanded their formularies to include anti-obesity medications, many still have “Weight Loss Exclusions.” This means that even if the drug is medically necessary, the plan specifically refuses to pay for weight management treatments.

To find out if glp-1 is covered by insurance under your specific plan, you must look at your Pharmacy Benefit Manager (PBM) formulary. Look for Wegovy, Zepbound, or Saxenda. If they are listed as “Tier 2” or “Tier 3,” they are likely covered but require a Prior Authorization. If you see “NC” or “Not Covered,” don’t panic there are still ways to fight this, including employer opt-ins or clinical exception appeals. Understanding the medical value of GLP-1s is your strongest argument in these appeals.

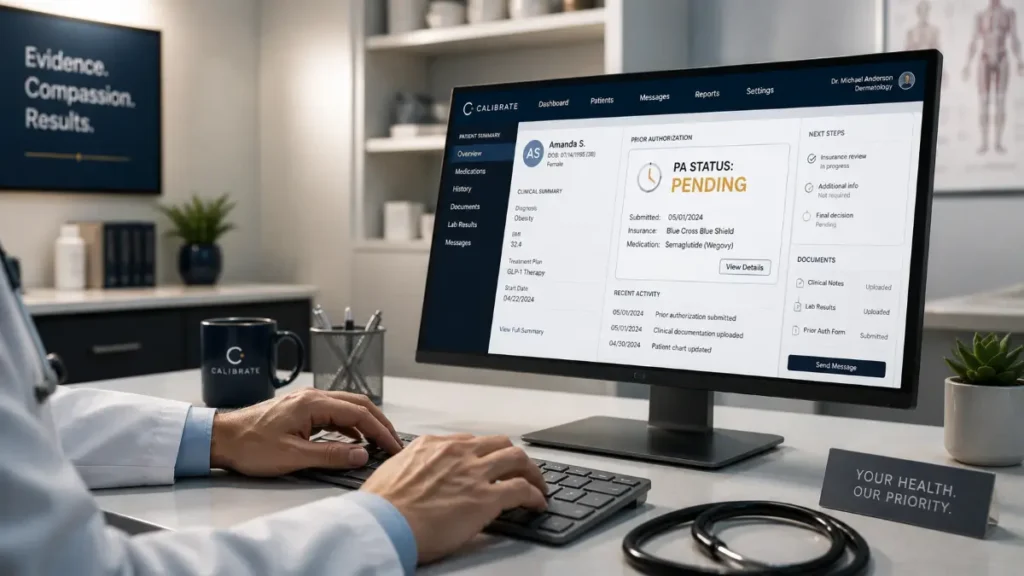

The prior authorization (PA) checklist

To get a glp-1 covered by insurance, your doctor must submit a Prior Authorization request. This is essentially a document proving to the insurance company that you meet their strict clinical criteria. In 2026, most insurance providers require the following:

- BMI requirements: A BMI of 30 or greater, OR 27 or greater with at least one weight-related comorbidity (e.g., high blood pressure, type 2 diabetes, high cholesterol).

- Step therapy: Proof that you have tried and failed a comprehensive lifestyle program (like a specific nutritional protocol) or cheaper weight loss medications for at least 3-6 months.

- Medical documentation: Recent blood work and a documented history of obesity-related health issues.

| Insurance Type | Typical Coverage Level | PA Difficulty |

|---|---|---|

| Commercial (Employer) | Varies (50% coverage rate) | Moderate |

| Medicare Part D | Low (Covers for heart health) | High |

| Medicaid | State Dependent (Rising) | Low/Moderate |

| TRICARE | High (Strict criteria) | Moderate |

How to appeal a denial: the 3-step strategy

If your initial request for glp-1 covered by insurance is denied, do not give up. Over 50% of first-time denials are overturned on appeal. Use this transparent strategy to fight back:

Step 1: Understand the reason. Was it “Lack of Medical Necessity” or “Plan Exclusion”? If it’s a plan exclusion, an appeal is much harder. If it’s medical necessity, you simply need more data.

Step 2: The Letter of medical necessity (LMN). Have your doctor write a detailed LMN highlighting your unique health risks. Mention any cosmetic side effects you are willing to manage if it means improving your cardiovascular health. In 2026, insurance companies are more likely to approve drugs if they believe it will prevent a $50,000 heart surgery later.

Step 3: External Review. If your second appeal is denied, you have the legal right to an Independent External Review. A third-party medical professional will review your case, and their decision is binding for the insurance company.

Employer opt-Ins: the secret backdoor

Many people don’t realize that their employer actually decides what the insurance covers. If your glp-1 is not covered by insurance, it may be because your company’s HR department opted out of weight loss coverage to save money.

You can advocate for yourself by speaking with HR. Many companies in 2026 are adding GLP-1 coverage because they see the benefits: lower absenteeism, higher productivity, and lower long-term disability costs. We provide templates for these conversations in our comprehensive cost guide.

Getting your glp-1 covered by insurance is possible with the right approach. Be your own advocate, work closely with your doctor, and don’t be afraid of the appeal process.

- ✅ Check: Verify your PBM formulary before your doctor’s appointment.

- ✅ Prepare: Have your BMI and comorbidity data ready for the PA request.

- ✅ Fight: Always appeal at least twice if denied.

You are fighting for a healthier, longer life. That is a battle worth winning. If insurance still fails, remember that compounded options are a safe and affordable fallback. Ready to find a local clinic? See our guide on injections near you.